Tax audits carried out by Poland’s National Revenue Administration (Krajowa Administracja Skarbowa, KAS) now look very different from how they did just a few years ago. They are becoming less broad and random, and increasingly precise, data-driven and based on risk assessment and digital reporting tools. For businesses, this marks an important shift: tax risk in Poland no longer depends only on the substance of a tax settlement, but also on data quality, process consistency and the organisation’s readiness to explain potential discrepancies quickly when approached by the authorities. The strategic direction of KAS for 2025–2028 explicitly highlights further development of analytics, digitalisation and more accurate targeting of audit activity.

In practice, this means businesses should no longer view preparation for a tax audit in Poland as an emergency response. It should instead be treated as part of ongoing tax risk management, supported by regular tax advisory in Poland. This applies both to larger organisations and to medium-sized businesses, especially those operating in environments with a high volume of documents, VAT reporting, domestic and international transactions, or more complex accounting structures.

The digitalisation of tax reporting is making audits more effective

The growing effectiveness of Poland’s National Revenue Administration (KAS) is not only the result of more enforcement activity. The key change is that the authorities now have access to broader data sets and can match, analyse and compare them much faster. This operating model is being strengthened by the continued digitalisation of tax reporting in Poland.

From 1 February 2026, the implementation phase of mandatory National e-Invoicing System (KSeF) in Poland began, although the exact deadline depends on the taxpayer’s status and the type of activities performed. KSeF means further standardisation of invoice data and greater transparency of business transactions from the perspective of the Polish tax authorities. This does not mean, however, that every invoice in every case is subject to the same rules. In practice, businesses should review their invoicing processes against their actual operating model.

At the same time, JPK reporting obligations in income taxes are also being developed further. This does not mean that all taxpayers are simultaneously covered by JPK_CIT reporting. Instead, the new requirements for submitting tax books and records are being introduced gradually. According to information from the Ministry of Finance, the first group covered includes the largest Corporate Income Tax (CIT) taxpayers, including entities with revenue exceeding EUR 50 million and tax capital groups, while further groups of taxpayers are being included step by step in the following years. The first JPK_KR_PD structures are expected to be submitted in 2026 for a financial year beginning after 31 December 2024. In addition, some structures were temporarily covered by executive exemptions.

This is highly relevant from a business perspective. Under the new audit model, tax risk in Poland often no longer results only from an incorrect interpretation of a legal provision. The source of the problem may also be inconsistencies between accounting books and tax returns, uncoordinated document flows, data mapping errors, manual adjustments without proper justification, or accounting systems that are not ready for the new reporting obligations. That is why well-organised accounting services in Poland are becoming increasingly important.

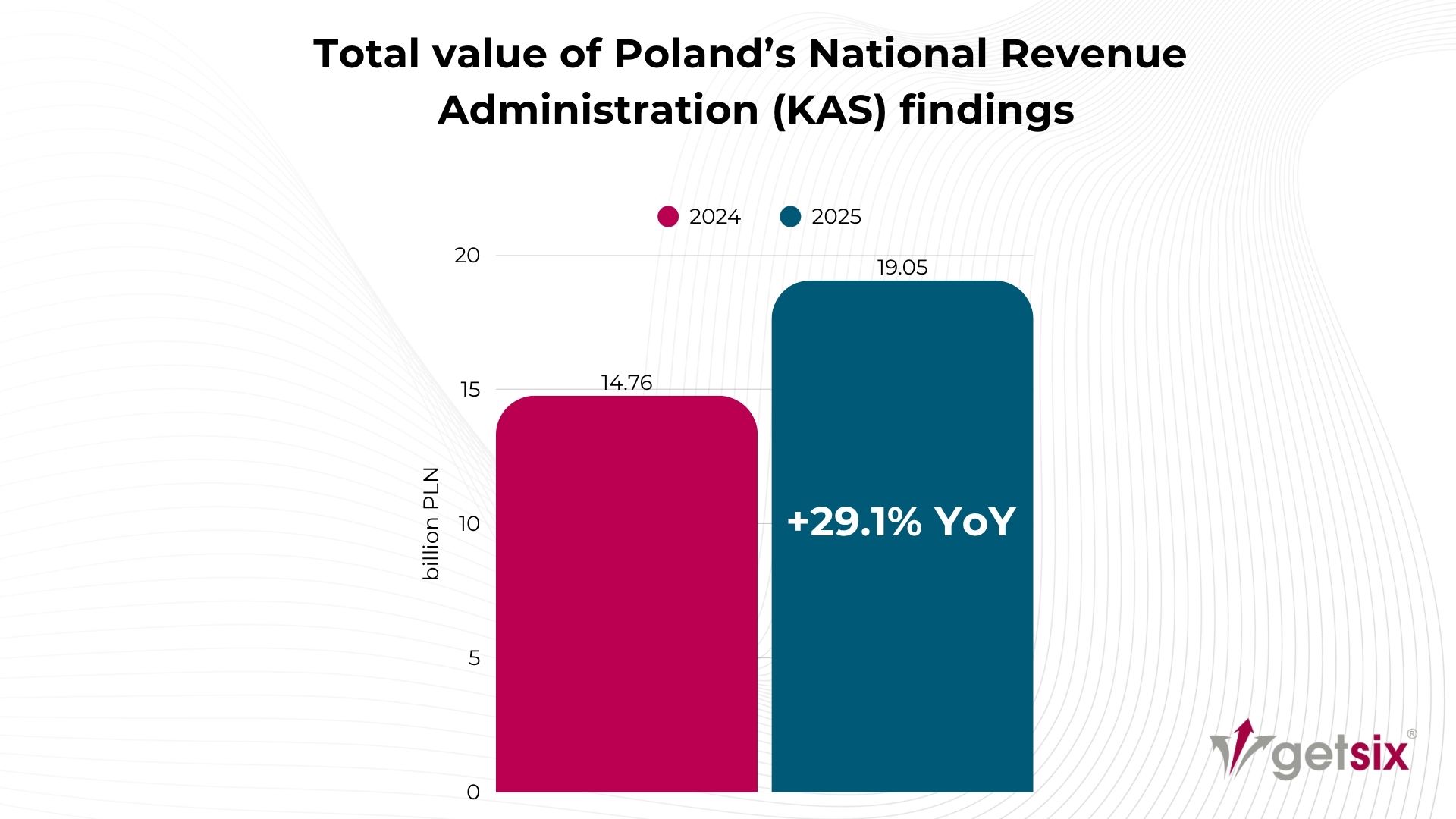

2025 figures show a clear increase in the effectiveness of Polish tax audits

The strongest argument confirming the changing operating model of Poland’s National Revenue Administration (KAS) comes from the official 2025 figures. KAS reported that, as a result of customs and fiscal audits, tax audits and verification activities, the total value of findings increased by 29.1% year on year, from PLN 14.76 billion in 2024 to PLN 19.05 billion in 2025. At the same time, the total number of actions increased by 9.4%, from more than 2.41 million to nearly 2.64 million.

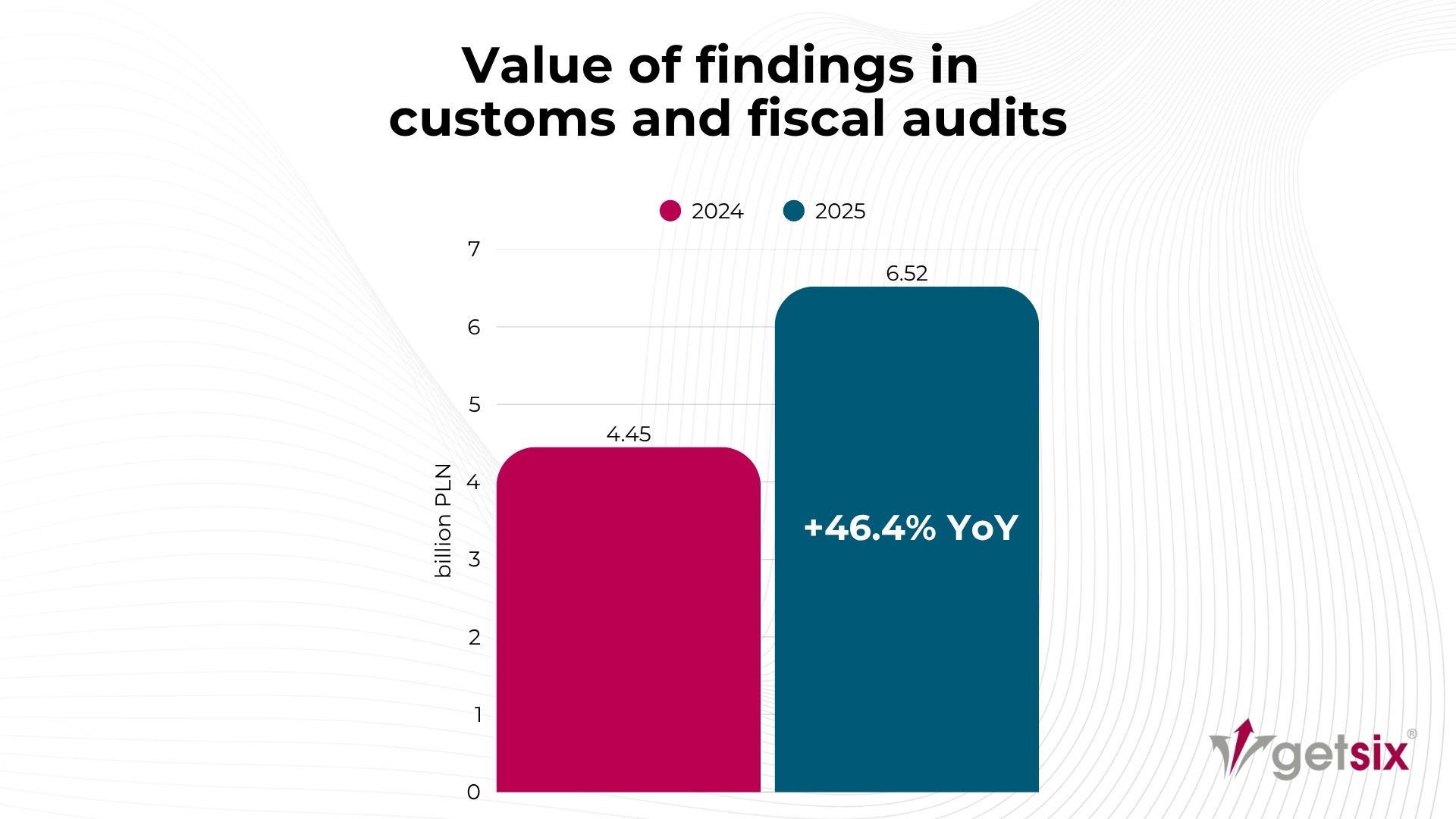

An even clearer signal can be seen in customs and fiscal audits. In 2025, the number of such audits fell from 7,043 to 5,113, or by 27.4%, yet the value of findings increased from PLN 4.45 billion to PLN 6.52 billion, or by 46.4%. This combination of figures is difficult to interpret in any other way than as confirmation of more accurate targeting and more effective risk analysis before the most formal audit procedures are opened.

A similar direction is visible in standard tax audits. Their number fell by 11.3%, from 9,829 in 2024 to 8,722 in 2025. The administration is clearly shifting more of its focus towards earlier, faster and less formal forms of action, while a traditional tax audit is increasingly reserved for situations where the authority considers it genuinely necessary.

Comparing 2024 and 2025: what actually changed

A comparison of 2024 and 2025 leads to several important conclusions.

First, the increase in findings was not simply the result of a higher number of standard audits. On the contrary, in some formal areas there were fewer actions, yet their financial impact was greater. This suggests that Poland’s National Revenue Administration (KAS) is becoming increasingly effective at identifying high-risk entities and areas before a full audit begins.

Second, analytical activities and verification procedures are becoming more important. For businesses, this means that contact with the authorities may happen earlier and in a less formal form, but this does not make the issue any less serious.

Third, companies must now be better prepared to demonstrate consistency in their data. In the reality of digitally analysed tax settlements, separate reporting obligations can no longer be treated in isolation. Data from accounting books, tax returns, VAT records and invoices increasingly forms one coherent picture of the taxpayer’s activity in Poland.

Verification activities are now more important than before

Poland’s National Revenue Administration (KAS) has clearly stated that verification activities are the fastest and least burdensome form of action from the taxpayer’s perspective. In 2025, their number increased by 9.6%, while the amounts identified at this stage rose by almost 28%, or by more than PLN 2.4 billion compared with 2024.

For businesses, this has a very practical consequence. More and more often, a tax issue in Poland does not begin with the formal launch of an audit, but with a request to submit explanations, present documents or justify a specific tax treatment. This stage is less formal, but from a tax risk management perspective it should not be underestimated. This is often the point at which a company needs to determine quickly what the authority is questioning, what data the administration already has, and whether the discrepancy is isolated or systemic.

From the taxpayer’s perspective, this also means that communication with the authority must be managed consciously. Not every response prepared under time pressure will be equally safe. In many cases, documentation should first be organised properly and the company should establish who is responsible internally for particular areas of explanation.

Record detection of fictitious invoices confirms the growing role of analytics

One of the clearest indicators of the effectiveness of Poland’s National Revenue Administration (KAS) is the data on fictitious invoices. In 2025, the authorities detected 376,800 such invoices, 29.2% more than a year earlier. Their value exceeded PLN 10.9 billion, compared with PLN 8.71 billion in 2024. According to KAS, this was the highest level of detection since 2017.

For honest businesses, this is not only information about the fight against tax fraud. It is also a signal that due diligence is becoming increasingly important when selecting business partners, verifying documents and confirming the actual course of transactions in Poland. A formal accounting document alone may not be enough if the authority has doubts about the economic substance of a transaction or the actual performance of a service.

Poland’s National Revenue Administration (KAS) is targeting high-risk sectors and business models more accurately

According to KAS data, the sectors most frequently audited in 2025 included:

- gastronomy,

- construction,

- car repair workshops,

- the beauty industry,

- e-commerce.

These sectors have remained under closer scrutiny for years due to the higher risk of irregularities, high turnover of entities, the nature of payments or the structure of settlements.

This does not mean, however, that businesses in other sectors can treat the issue as relevant only to selected industries. In practice, selection for verification is increasingly driven not by the business classification itself, but by the data profile. Relevant factors may include unusual adjustments, non-standard profitability, repeated discrepancies in tax returns, transactions with related parties, extensive international transactions, or inconsistencies between accounting books and tax reporting.

Tax audits now serve a primarily preventive function

In this environment, a tax audit in Poland is no longer merely a tool for identifying errors after the fact. It is increasingly preventive, because it allows businesses to identify weak points in settlements and processes before the tax authority does.

A properly conducted audit helps assess whether a company:

- keeps its tax settlements consistent with accounting data,

- is prepared to present documents and explanations quickly,

- manages adjustments and process exceptions properly,

- has a clear allocation of responsibilities in the tax area,

- recognises areas of increased risk in CIT, Value Added Tax (VAT), withholding tax (WHT) or transfer pricing.

The National e-Invoicing System (KSeF) in Poland and JPK income tax reporting increase the importance of data quality

The most important change for businesses today is that reporting data is becoming part of an increasingly coherent information ecosystem. KSeF, JPK_VAT and the developing JPK structures in income taxes mean that the administration can identify discrepancies more quickly, compare data from different sources and direct questions more effectively to specific taxpayers.

In practice, businesses should verify not only whether a tax return has been submitted correctly, but also whether:

- source data is complete and recorded consistently,

- the accounting system accurately reflects actual business processes,

- corrections are properly documented,

- the flow of information between sales, accounting, tax and management teams does not create inconsistencies.

In many cases, it is precisely in these areas that risk arises and is later detected by KAS analytics.

Complex and cross-border tax settlements require particular attention

In practice, a higher risk of audit or deeper verification often concerns not only standard VAT settlements, but also such areas as transfer pricing, withholding tax, intra-group financing, intangible services or cross-border settlements. As analytics gains importance, formal correctness of documentation alone is becoming less sufficient. What also matters is consistency between documentation, accounting books, group policies and the actual course of the transaction.

In such cases, ongoing tax advisory in Poland becomes particularly important, as it helps businesses assess not only the formal correctness of tax settlements, but also the consistency of documentation, accounting records and the real substance of transactions. Support in this area helps identify risks earlier and prepare the company better for possible verification.

Better audit preparation also means better business management

It is worth emphasising that a tax audit and preparation for a tax inspection in Poland are not only defensive measures. In many organisations, they also bring operational and managerial value. Reviewing tax settlements helps streamline document flows, reduce manual operations, clarify responsibility for specific areas and improve the quality of reporting data.

This translates not only into a lower risk of tax positions being challenged by the authorities, but also into greater predictability of the tax outcome, better control over cash flow and a higher standard of internal oversight over the tax function. In a context where management boards are facing growing responsibility for tax matters, this has not only operational significance, but also evidential value.

What businesses should do in 2026

In an environment where tax audits by Poland’s National Revenue Administration (KAS) are becoming increasingly effective, companies should adopt a systematic approach.

First, they should verify the consistency of data across accounting books, tax returns, registers and source documents. Next, they should identify areas of elevated risk, especially where the company uses more complex tax treatments, frequent adjustments, group structures or cross-border transactions. Finally, internal procedures should be organised so that the business knows how to respond to questions from the authorities, who is responsible for preparing data and how explanations are documented.

This approach is now significantly safer than waiting to see how the situation develops and reacting only after a verification procedure or audit has already started.

FAQ

Does the growing effectiveness of Poland’s National Revenue Administration (KAS) mean there will be more tax audits?

Not necessarily. The 2025 data suggests rather that KAS is becoming better at selecting entities for verification. In some areas, the number of audits fell while their financial effectiveness increased. This points to greater selectivity rather than simply a higher number of actions.

Are verification activities less important than a formal tax audit?

No. They are less formal, but they may be the first sign that the authority has identified an irregularity or a discrepancy in the data. From a business perspective, they require an equally serious organisational response.

Does the National e-Invoicing System (KSeF) in Poland mean that the tax office has full access to all invoices without exception?

This should not be oversimplified. KSeF significantly increases the standardisation of and access to invoice data, but Polish regulations also provide for certain exclusions and special rules in some situations. That is why compliance obligations should always be assessed in light of the company’s specific operating model.

Does JPK_CIT already apply to all companies in Poland?

No. Income tax reporting obligations are being introduced in stages. Initially, they apply to selected groups of CIT taxpayers, while additional entities will be covered in later years. Each company should therefore verify its own status under the current Polish regulations and implementation timetable.

When is the right time to carry out a tax audit?

Ideally before entering a new reporting phase, after system changes, before year-end closing, after a business reorganisation, or when the company has cross-border settlements, related-party transactions or operates in a higher-risk sector.

Should small and medium-sized companies also prepare for tax audits by Poland’s National Revenue Administration (KAS)?

Yes. The size of the business does not eliminate risk if the data contains inconsistencies, unusual adjustments or mismatches between documents and tax settlements. In practice, smaller businesses may also be selected for verification based on data analysis.

The 2025 data clearly shows that tax audits by Poland’s National Revenue Administration (KAS) are becoming more selective, analytical and effective. A decline in the number of some formal audits combined with a higher value of findings confirms that the administration is making better use of risk analysis and digital data when selecting cases.

For businesses, this means the need to change their approach to tax risk in Poland. The safest solution today is not passive waiting, but earlier organisation of settlements, processes and documentation. In practice, preparation before contact with the authority is often what determines whether a case can be clarified quickly or turns into a costly and lengthy dispute.

{kind=link}